1. Introduction

The Plan is required to produce a yearly statement to describe how governance requirements have been met in relation to:

- the investment options in which members’ funds are invested (this means the default arrangements and other funds members can select or have assets in, such as “legacy” funds);

- the requirements for processing financial transactions;

- the charges and transaction costs borne by members;

- an illustration of the cumulative effect of these costs and charges;

- a ‘value for members’ assessment; and

- Trustee knowledge and understanding.

This statement has been prepared in accordance with the Occupational Pension Schemes (Charges and Governance) Regulations 2015 and covers the period 1 January 2019 to 31 December 2019.

2. The default lifecycle arrangements

The Plan has an Auto Enrolment section, which is used as a Qualifying scheme for auto-enrolment, and the Money Purchase 2003 section, which is not. Together these are the Defined Contribution (‘DC’) sections of the Plan. Members who do not opt in to, or are not eligible for the Money Purchase 2003 section are auto-enrolled into the Auto-enrolment section. Members of both sections are given the same investment choices and have the same default investment strategies.

Some members of the DC Sections of the Plan make their own investment choices from the range of investment options made available by the Trustee, but those who do not make an explicit choice regarding the investment of their funds are placed automatically into a default lifecycle arrangement. After taking advice, the Trustee decided to make the default lifecycle arrangements, which means that members’ assets are automatically moved between different investment funds within the default lifecycle arrangement as they approach their target retirement date.

There are three separate default lifecycle strategies, the ‘Drawdown Lifecycle’, the ‘Cash Lifecycle’ and the ‘Annuity Lifecycle’. Details of how members contributions are invested into the different default lifecycle strategies are set out below.

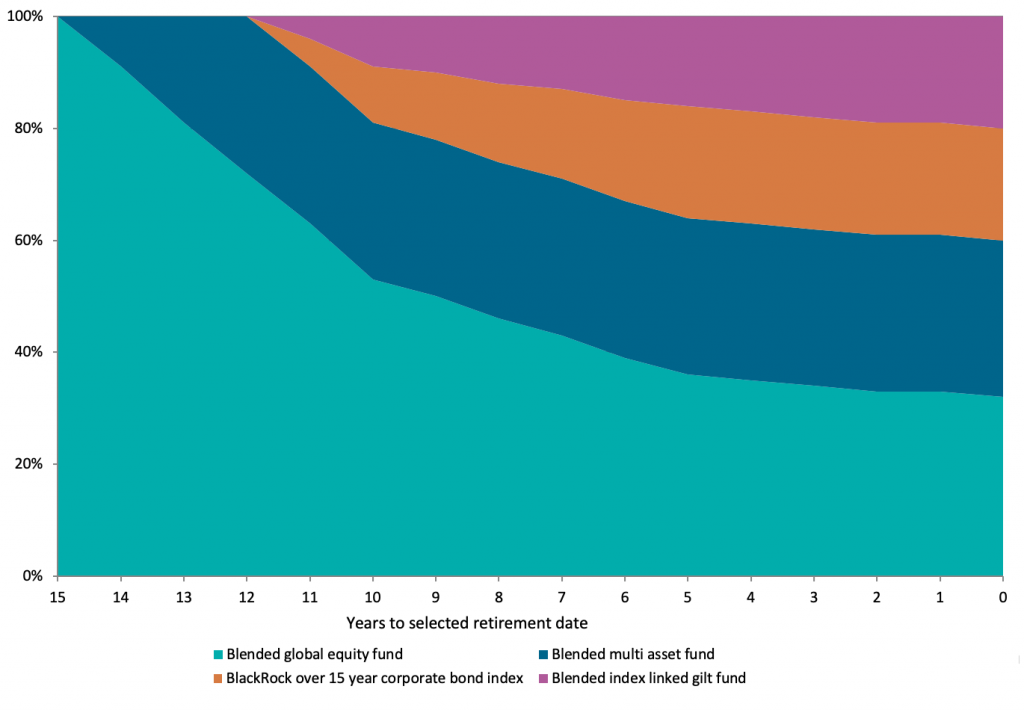

Where an explicit choice has not been made by the member, contributions into the DC sections are invested into the ‘Drawdown Lifecycle’. The asset allocations in the years leading up to retirement for the Drawdown lifecycle is shown below:

Members who make additional voluntary contributions (AVCs) have the same investment fund choices, but if they do not make an explicit choice their AVC assets are placed into the ‘Cash Lifecycle’, which is the default arrangement for AVCs. The asset allocations in the years leading up to retirement for the Cash lifecycle is shown below:

The Plan also has a legacy default lifecycle arrangement, the ‘Annuity Lifecycle’, into which the assets of a number of members close to retirement were transferred into as part of the last investment strategy review. The asset allocations in the years leading up to retirement for the Annuity lifecycle is shown below:

The Trustee is responsible for investment governance, which includes setting and monitoring the investment strategy for the default lifecycle arrangements.

Details of the objectives and the Trustee’s policies regarding the default arrangements can be found in a document called the ‘Statement of Investment Principles’ (“SIP”), which can be found here: https://www.pearson-pensions.com/go/statement-of-investment-principles

The objective of the default lifecycle arrangement, as stated in the SIP, is as follows:

“The objective of the main default option for the DC sections, the Drawdown Lifecycle, is to generate returns significantly above inflation whilst members are some distance from retirement, but then to switch automatically and gradually to lower risk investments as members near retirement.”

The objectives of the Cash default arrangement and the annuity default arrangements, as stated in the SIP, are as follows:

“The aim of all the default Lifecycle strategies (specifically the Cash and Annuity strategies) is to provide members with the potential for higher levels of growth during the accumulation of their retirement savings though exposure to equity and diversified growth funds and then to gradually diversify their investments in the years approaching retirement, in order to reduce volatility while still providing suitable exposure to growth assets. The asset allocation throughout the default Lifecycle strategies and the phasing of the gradual switching of investments takes into account members’ greater capacity for risk early on and reduced capacity for risk in later years.

In the initial growth phase, the above lifecycle options (including the legacy default, the Annuity Lifecycle) are invested to target a return significantly above inflation, and then in the 15 years before retirement, they switch gradually into less risky assets, with the asset allocation at retirement being designed to be appropriate for members wishing to access drawdown (in the case of the Drawdown Lifecycle), take their pot as cash (the Cash Lifecycle) or purchase an annuity at retirement (Annuity Lifecycle).”

The default lifecycle arrangements are described below and each of the asset allocation tables can be found at https://www.pearson-pensions.com/library/#booklets.

The Trustee considers these approaches to be in the best interest of relevant members and relevant beneficiaries. The default lifecycle arrangements meet the requirements for social environmental and governance considerations set out in the SIP.

Whilst outside of the Plan year, the Threadneedle Pensions Property Fund was suspended by the manager in May 2020 due to pricing uncertainty caused by the Covid-19 crisis. Member contributions are being redirected into the BlackRock Sterling Liquidity Fund until such time as the Property Fund can reopen. As members’ contributions are being directed into the BlackRock Sterling Liquidity Fund without them making an active selection, this fund will be treated as a default for the purpose of fulfilling legislative requirements. The aims and objectives of the strategy are that the fund aims to maximise current income consistent with the preservation of capital and liquidity through the maintenance of a portfolio of high quality short-term “money market” instruments and to achieve an investment return that is in line with its benchmark.

On a quarterly basis after charges the performance of funds (which can be found below) comprising the default lifecycle arrangements are reviewed by the Investment Committee. Throughout the year ended 31 December 2019, investment returns for passive funds have generally tracked benchmarks, and have performed in accordance with the objectives of the fund as set out in the SIP. The performance of the active funds within the lifecycle arrangements has been more varied, which is expected as the benchmark is less likely to be an exact match for the fund given the active management. Where performance is not in line with benchmarks or objectives, the Investment Committee have investigated the underperformance with the investment consultants and investment managers in order to establish if any further action is necessary. The reviews that took place during the year concluded that the default lifecycle arrangements were performing broadly as expected and so no changes were made to the underlying funds that make up the lifecycle arrangements.

The default lifecycle arrangements are formally reviewed to assess the ongoing suitability and strategy of the default lifecycle arrangement at least every three years or immediately following any significant change in investment policy or the Plan’s membership profile. The default lifecycle arrangements were not formally reviewed during the period covered by this Statement. The last review took place over the course of several meetings, with final decisions being taken by the Investment Committee at its meeting on 3 October 2017. The performance and strategy of the previous default arrangement, the ‘Annuity Lifecycle’ were reviewed to ensure that investment returns (after deduction of any charges) had been consistent with the aims and objectives of the default lifecycle arrangement as stated in the SIP, and to check that it continues to be suitable and appropriate given the Plan’s risk profiles and membership.

The resulting investment transition took place in April 2018, and included the creation of the current three lifecycle arrangements. The default lifecycle arrangement for contributions into the DC sections of the Plan was amended from the Annuity Lifecycle which had targeted the purchase of an annuity at retirement, to the Drawdown Lifecycle which targets a drawdown option being taken at retirement. This was in response to the trends the Plan was seeing in the options its members were taking on retirement following the pension freedoms allowed under the Pensions Act 2014 and due to high annuity prices. The performance after charges of the funds selected as part of these changes were consistent with the objectives in the SIP. The range of self-select investment funds was also revised at that time.

Following the investment transition, the Trustee is satisfied that the default lifecycle arrangements were appropriate based on the Plan’s membership profile. The next full triennial review of the investment arrangements is due to take place in September 2020.

3. Core financial transactions

The Trustee has a specific duty to secure that core financial transactions (including the investment of contributions, transfer of member assets into and out of the Plan, transfers between different investments within the Plan and payments to and in respect of members) relating to the DC Sections are processed promptly and accurately.

The Trustee delegates responsibility for this to the staff of the Plan and the Plan’s DC provider, Aviva. The agreement the Trustee has in place with Aviva incorporates specific service level agreements (SLAs) which include targets for the accurate and timely processing of core financial transactions. The Trustee monitors the performance against these SLAs via quarterly reports.

The staff of the Plan and Aviva have set up various controls to ensure the accuracy of processing core financial transactions, for example:

- a reconciliation to ensure all contributions were processed using monthly Aviva reporting data;

- a reconciliation of monies disinvested for member refunds to amounts returned to the Plan by Aviva; and

- an annual reconciliation of membership using data supplied from Aviva against membership held on the pension administration database.

The Trustee has received assurance from the Plan’s DC provider, Aviva, and from management reporting that they have adequate internal controls, including review procedures, and inbuilt automated controls within their systems, to ensure that core financial transactions relating to the Plan were processed promptly and accurately during the year. Any issues identified by the Trustee as part of its review processes (set out below) would be raised with the administrators immediately, and steps would be taken to resolve the issues.

The processes the Trustee has in place for monitoring of core financial transactions are as follows:

- Review of quarterly SLA reporting from Aviva, covering reporting on each type of transaction for number of cases processed, and how many days each has taken. It has been noted that throughout the year there have been instances where the performance has fallen below target. In response to this, management have worked closely with Aviva, and several measures have been put in place to rectify the issues, including a restructuring of the Aviva team.

- Review of quarterly management reporting against agreed SLAs from management, detailing what activities have taken place, and what, if any, exceptions have occurred.

- The Trustee have appointed the Audit and Risk Committee to review the Breaches Register half yearly, where any statutory or legal breaches would be reported.

- External auditors perform some limited controls testing for the purposes of their statutory audit and report back any issues via their Management report.

Based on its review process, the Trustee is satisfied that over the period covered by this statement:

- both the Plan and the DC provider were operating appropriate procedures, checks and controls and operating within the agreed SLAs;

- there have been no material administration errors in relation to processing core financial transactions; and

- Whilst SLA performance has at times been lower than the SLA target (as noted above), the Trustee is satisfied that this is being addressed and will continue to monitor performance of Aviva’s services over the remainder of 2020 and into 2021.

4. Member-borne charges and transaction costs

Regulations also require the Trustee to make an assessment of ongoing charges borne by members of the DC Sections and the extent to which those charges and costs represent good value for members.

These are annual fund management charges plus any additional fund expenses, such as custody costs, but excluding transaction costs; this is also known as the total expense ratio (“TER”). The TER is paid by the members and is reflected in the unit price of the funds. The stated charges include administration costs, since these are met by the member.

The Trustee is also required to separately disclose transaction cost figures that are borne by members. In the context of this Statement, the transaction costs shown are those incurred when the Plan’s investment managers buy and sell assets within investment funds but are exclusive of any costs incurred when members invest in and switch between funds. The transaction costs are borne by members.

The charges and transaction costs have been supplied by Aviva (the Plan’s platform provider), and by the Plan’s legacy AVC providers. When preparing this section of the Statement the Trustee has taken account of the relevant statutory guidance. Due to the way in which transaction costs have been calculated it is possible for figures to be negative; since transaction costs are unlikely to be negative over the long term the Trustee has shown any negative figure as zero.

4.1 Default arrangements

The default arrangement for the MP03 and Auto-enrolment sections is the Drawdown lifecycle arrangement. For the period covered by this Statement, annualised charges and transaction costs are set out in the following table:

The default arrangement for AVC contributions is the Cash lifecycle arrangement. For the period covered by this Statement, annualised charges and transaction costs are set out in the following table:

The Annuity lifecycle arrangement is a legacy lifecycle arrangement, for the period covered by this Statement, annualised charges and transaction costs are set out in the following table.

The TER for all three of these arrangements are much lower than the maximum allowed of 0.75% and the Trustee is satisfied that it has negotiated good terms for members taking account of the expected growth in the size of the DC Sections.

4.2 Self-select options

In addition, there is a range of 11 separate funds which may be chosen by members as an alternative to the default lifecycle arrangement. These funds allow members to take a more tailored approach to managing their own pension investments.

Annual management charges for each fund for 2019 are shown below, but current charges can also be found on the Plan’s website at www.pearson-pensions.com/library. The underlying funds used within the default arrangement are shown in bold.

Legacy AVC fund charges and transaction costs

The following funds were available to members as legacy options for Additional Voluntary Contributions. These options are now closed to future contributions.

*There is no explicit charge. The contractual Guaranteed Investment Return of 3.5% pa is applied following the deduction of the current charge of 1.0% for the costs of administration and 0.5% pa for the costs of guarantees.

** There are no explicit charges for these funds, but charges are deducted before the bonus is declared. The Trustee is working with the provider to confirm these charges.

***The Trustee is working with the provider to confirm which funds the Plan has assets invested in / or and the charges for these funds.

Whilst TER and transaction cost data for the majority of the funds available to members has now been obtained, the Trustee will continue to work with its advisers to gain the most up to date transaction cost information for any remaining funds. The Trustee’s advisers will continue to liaise with the AVC providers to attempt to obtain this information by requesting this information on a regular basis.

Following the year end, Equitable Life sold its book of business to Utmost Life and Pensions. The Trustee has received advice in relation to this sale and members were transferred into the Cash Lifecycle within the AVC section of the Plan in June 2020.

4.3 Illustration of charges and transaction costs

The illustrations show how different costs and charges can impact the pension pot over certain periods of time, based on a selection of investment funds. Statutory guidance from The Pensions Regulator has been taken into account in the preparation of these illustrations. Under each default lifecycle arrangement or investment fund, there are two columns. The first shows the projected pension values assuming no charges are taken. The second shows the projected pension values after costs and charges are taken. By comparing the two you can see how much the charges over the years will impact your pension fund.

The “before costs” figures represent the savings projection assuming an investment return with no deduction of member borne charges or transaction costs. The “after costs” figures represent the savings projection using the same assumed investment return but after deducting member borne charges (ie the TER) and an allowance for transaction costs.

The transaction cost figures used in the illustration are those provided by the managers over the past two years, subject to a floor of zero (so the illustration does not assume a negative cost over the long term). We have used the average annualised transaction costs over the past two years as this is the longest period over which figures were available, and should be more indicative of longer-term costs compared to only using figures over the Plan year.

The illustration is shown for the Drawdown Lifecycle, since this is the arrangement with the most members invested in it, as well as the two alternative lifecycles, the AVC default (the Cash Lifecycle) and the legacy default (the Annuity Lifecycle) and also four funds from the Plan’s self-select fund range.

The four self-select funds shown in the illustration are:

- the fund with the highest before costs expected return – this is the BlackRock UK Equity Index Fund

- the fund with the lowest before costs expected return – this is the BlackRock Institutional Sterling liquidity Fund

- the fund with highest annual member borne costs – this is the Jupiter Ecology Fund

- the fund with lowest annual member borne costs – this is the Blended Index Linked Gilt Fund

Illustration of effect of costs and charges for typical funds within the Plan

Projected pension pot in today’s money

Projected pension pot in today’s money

Notes

- Values shown are estimates and are not guaranteed. The illustration does not indicate the likely variance and volatility in the possible outcomes from each fund. The numbers shown in the illustration are rounded to the nearest £100 for simplicity.

- Projected pension pot values are shown in today’s terms, and do not need to be reduced further for the effect of future inflation.

- Annual salary growth and inflation is assumed to be 2.5%. Salaries could be expected to increase above inflation to reflect members becoming more experienced and being promoted. However, the projections assume salaries increase in line with inflation to allow for prudence in the projected values.

- The starting pot size used is £800. This is the approximate average (median) pot size for active members aged 25 years and younger (as these members can be expected to have around 40 years to retirement)

- The projection is for 40 years, being the approximate duration that the youngest Plan member has until they reach the Plan’s Normal Pension Age.

- The starting salary is assumed to be £22,000. This is the approximate median salary for active members aged 25 or younger.

- Total contributions (employee plus employer) are assumed to be 8.0% of salary per year. This is the median total contributions for active members aged 25 or younger.

- The projected annual returns used are as follows:

- Drawdown Lifecycle: 2.5% above inflation for the initial years, gradually reducing to a return of 1.3% above inflation at the ending point of the lifecycle.

- Cash Lifecycle: 2.5% above inflation for the initial years, gradually reducing to a return of 1.0% below inflation at the ending point of the lifecycle.

- Annuity Lifecycle: 2.5% above inflation for the initial years, gradually reducing to a return of 0.6% below inflation at the ending point of the lifecycle.

- BlackRock UK Equity Index Fund: 3.0% above inflation

- BlackRock Sterling Liquidity Fund: 1.0% below inflation

- Jupiter Ecology Fund: 3.0% above inflation

- Blended Index Linked Gilt Fund: 0.5% below inflation

- No allowance for active management outperformance has been made.

While these costs are important, they should not be looked at in isolation but should be viewed within the context of the performance of the fund or funds chosen as these costs are, ultimately, reflected in the performance of the fund.

5. Value for members assessment

The Trustee has assessed the extent to which member borne charges and transaction costs detailed above represent good value for money to members.

The Trustee reviews all member-borne charges (including transaction costs where available) annually, with the aim of ensuring that members are obtaining value for money given the circumstances of the Plan. The date of the last review was the date of this report, 23 June 2020. The Trustee notes that value for money does not necessarily mean the lowest fee, and the overall quality of the service received has also been considered in this assessment. The Trustee’s investment advisers have confirmed that the fund charges are competitive for the types of fund available to members.

The Trustee assesses the performance of the Plan’s investment funds (after all charges) in the context of their investment objectives on a quarterly basis. The returns on the investment funds members can choose during the period covered by this Statement have broadly been consistent with their stated investment objectives. Where the Trustee has any concerns that a fund is not providing returns in line with its objective, a review is carried out to assess whether any change is required, noting however, that short term performance is not used as a criteria for the Trustee to change an investment option.

In carrying out the assessment, the Trustee also considers the other benefits members receive from the Plan, which include (amongst other aspects):

- The design of the default lifecycle arrangements and how these reflect the interests of members.

- The range of investment options and strategies.

- The efficiency of administration processes, the quality of communications, support services and Plan governance, including the additional benefit of an in-house pensions team, solely focussed on the Plan’s arrangements.

- Access to retirement planning tools through the Aviva member site.

- Access to factsheets and guidance provided on the Plan website.

- Additional ill health and death benefits for Plan members.

- Access to additional discounts and benefits on a range of products with the Plan’s DC provider, Aviva.

Having taken advice from its investment advisers, the results of the Trustee’s assessment are as follows:

- Charges – Very good – Members bear the cost of administration charges but fees are reasonably competitive. The Trustee will look for opportunities to negotiate lower fees for members as part of the regular review process.

- Administration – Good – The administration services provided by Aviva are of a good standard. The Trustee is considering increasing its engagement with the administrator to improve performance relative to SLAs.

- Governance – Very good – The Trustee and pensions team are very committed to the Plan, demonstrated by the dedicated level of resources and commitment to training.

- Communications – Good – The Trustee and the administrator issues timely and relevant information to members.

- Default investment arrangement – Very good – The strategies broadly achieved their objectives over the year. The next review will be in September 2020.

- Investment range – Very good – The self-select fund range provides access to most asset classes, some specialist options and alternative lifestyle strategies.

- At-retirement services – Good – Support and guidance offered to members are reasonable.

- Plan design – Very good – The Plan’s design and contribution structure are reasonable and encourage members to take advantage of the extra matching contributions.

Having considered the various aspects of the Plan, the Trustee is comfortable that the Plan is offering good value to members for the costs and charges they incur and will continue to monitor this.

In addition to value provided by the Plan to members, members also benefit from employer contributions, which in the case of the Money Purchase 2003 Section, provides £2 of contributions by the employer for every £1 contributed by the employee, up to the employer contributing 16% of the employee’s salary, depending on age. Contributions provided by the employer for the Auto-enrolment section of the Plan are in line with legislation. Most members of the Auto-enrolment section have the option to switch into the Money Purchase 2003 section, subject to meeting eligibility criteria.

6. Trustee knowledge and understanding

The Plan’s Trustee is required to maintain appropriate levels of knowledge and understanding to run the Plan effectively. The Trustee has measures in place to comply with the legal and regulatory requirements regarding knowledge and understanding of relevant matters, including investment, pension and trust law. Details of how the knowledge and understanding requirements have been met during the period covered by this Statement are set out below.

As set out in the Trustee’s Report, a review of the governance of the Plan, including arrangements with respect to Defined Contribution members, their contributions and benefits, is undertaken by the Trustee through its board and committees.

The Trustee’s priority is to provide a strong and stable pension scheme which operates in the interests of its members and to achieve this the Trustee Board and its Committees meet regularly to develop and agree strategy, monitor performance, discuss and explore issues relevant to the governance and administration of the DC arrangements and make appropriate decisions.

The Plan’s Trustee Directors are required to maintain appropriate levels of knowledge and understanding to run the Plan effectively. Each Trustee Director must:

- Be conversant with the trust deed and rules of the Plan, the Plan’s statement of investment principles and any other document recording policy for the time being adopted by the Trustee relating to the administration of the Plan generally,

- have, to the degree that is appropriate for the purposes of enabling the individual properly to exercise his or her functions as trustee director, knowledge and understanding of the law relating to pensions and trusts and the principles relating to investment the assets of occupational pension schemes.

The Trustee has measures in place to comply with the legal and regulatory requirements regarding knowledge and understanding of relevant matters, including investment, pension and trust law. The Pensions Director aims to identify training needs on any topics that become relevant, as well as Trustee’s themselves raising any training needs informally in meetings and other communications, and more formally via the annual Trustee evaluation questionnaire. Any Trustee Knowledge & Understanding (TKU) requirements are shared with the Chairman each year, and incorporated into the Trustee Action Plan. As a result, during the year, the Trustee Directors have been provided with training on cyber security, and also received various legal updates from the Plan’s lawyers within Board Meetings, and have also undertaken individual training across a range of topics which has been recorded within TKU records held by the Pensions Director.

Documents and guidance with Plan specific information, including Plan Rules, are provided via the digital board book system to all Trustee Directors and Committee members. All changes to Plan rules are approved by the Trustee. Elements of the Plan Rules are regularly discussed in Trustee meetings. The SIP is available on the website

https://www.pearson-pensions.com/go/statement-of-investment-principles and is also regularly discussed in Trustee and committee meetings and reviewed at least annually.

All new Trustee Directors during the year have completed the Pension Regulator’s trustee toolkit, and have received detailed briefings from both the Pensions Director and key advisers, as well as other Plan staff as required, tailored to individuals’ existing knowledge and expertise.

The Trustee believes that the combined knowledge and understanding of the Trustee directors, the independent members of certain committees and the staff of the Plan, together with external advice where appropriate, enables the Trustee to exercise properly its functions by providing collectively experience of governance, pension fund management, administration, investment, finance, audit and member representation.

The Chairman’s Defined Contribution Governance Statement was approved by the Trustee on 3 July 2020 and signed on its behalf by:

J A B Joll

Chairman